Euro and German Bunds on the Rise

UST’ Status as the Global Reserve Asset of Choice

Trump Administration's new tariff policy has significantly increased the volatility not only in the equity markets but also in the bond markets, ultimately triggering a technical unwinding of billions of dollars by the highly leveraged hedge fund trades.

To be sure, if the sell-off of USTs is disorderly and destructive, it can cause grave danger to the entire financial markets.

We are talking about “Treasury Basis Trades”, where hedge funds with high leverage buy UST (long) and at the same time sell UST futures (short) and pocket the almost risk-free spread in petty basis points.

Since USTs are worldwide favoured as safe and liquid assets, speculative hedge funds replicate such trades several times with leverage. In other words, speculative investors can use the UST as collateral in exchange for short-term loans in the repo market, again and again.

The problem is that the prime brokers in the repo markets demand much more collateral when there is unusual volatility in the market.

And if the hedge fund can't jump on, the lenders can grab the collateral - government bonds - and sell them into the market. As a result, there is a major threat lurking in the market, which is supposed to be solid, because backed by high-quality Government bonds like the USTs.

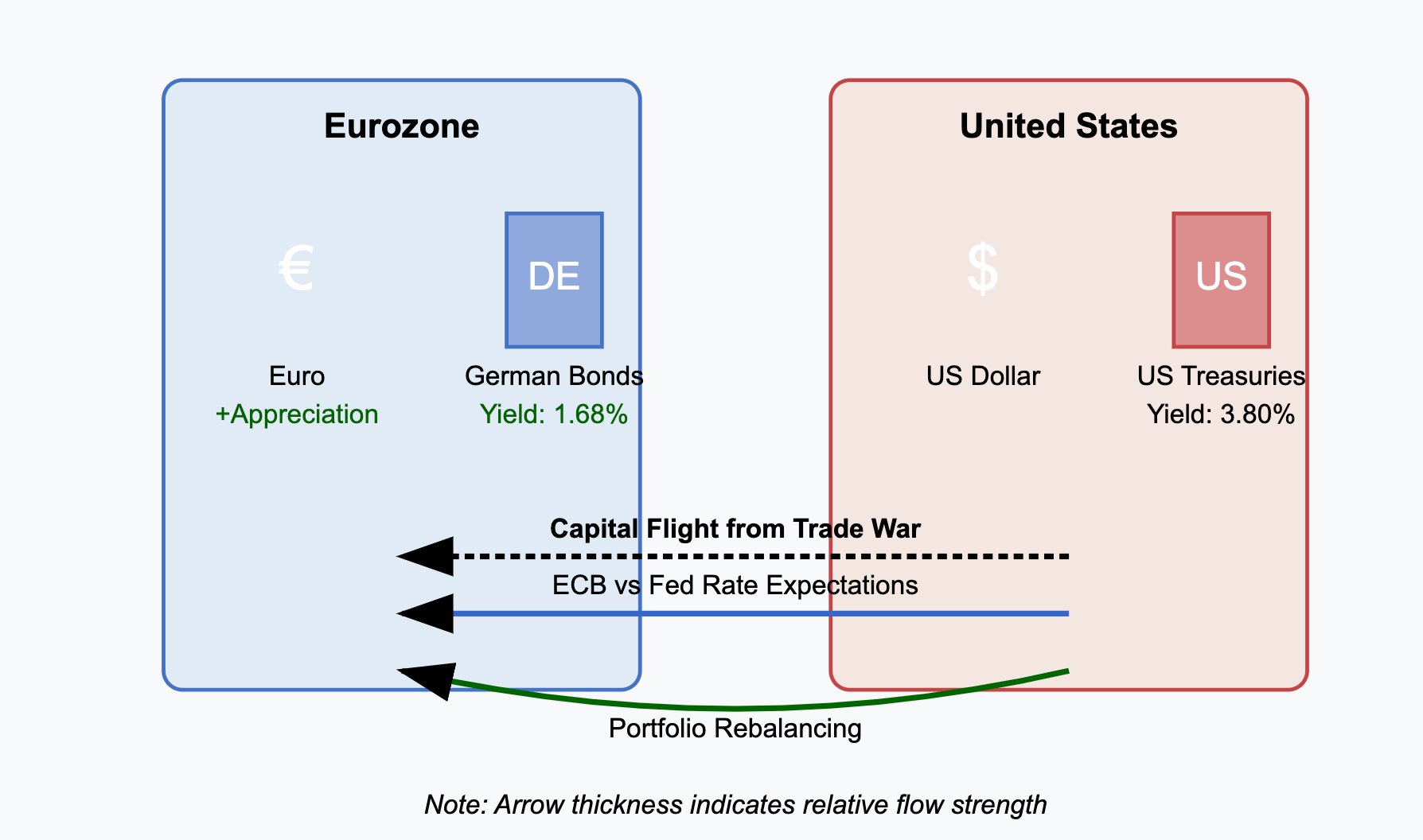

With this in mind, the simultaneous rise in the euro and German government bond prices (if prices are up, yields are down) is quite telling.

While capital flight and safe-haven demand amid trade war fears is a key reason, here are several other contributing factors that may be at play:

If markets expect the Fed to cut rates due to slowing growth or financial stress from a trade war:

- UST yields fall as investors price in lower future rates.

- Rate differentials narrow, making the euro relatively more attractive.

- Euro rises as capital shifts away from USD assets.

If recent economic data from the U.S. disappoints, while Eurozone surprises positively (e.g., stronger industrial production due to recently announced fiscal stimulus through Germany’s new incoming government) that:

- Improves sentiment toward the euro.

- Boosts demand for eurozone debt as a “less-bad” option.

Even within the eurozone, during uncertain times (e.g., trade disputes, geopolitical risk), investors often flee to German Bund as:

- They are considered the safest asset in the euro area.

- So, demand rises → prices rise → yields fall.

This can happen even if eurozone-wide sentiment isn't great.

Large institutions may buy euro bonds and hedge USD exposure, creating demand for euros. This can push up:

- Euro exchange rate.

- German bond prices if they’re being used for collateral or duration matching.

If investors believe that inflation in the U.S. will cool faster than in the eurozone, it might:

- Push down UST yields more aggressively.

- Increase the relative attractiveness of euro assets.

- Support euro appreciation (expectations of less aggressive ECB cuts).

Institutional investors (like pensions, insurance firms) might rebalance portfolios away from equities or risky EM debt into core eurozone debt, especially in volatile environments.

If the ECB recently struck a less dovish tone or hinted at being cautious on rate cuts:

- That would support both the euro and Bunds.

- Especially if compared with a Fed seen as more likely to ease.

If you've been following the recent sell-off in the US Treasury market, and you are particularly interested in understanding the relationship between the Supplementary Leverage Ratio (SLR) requirements and this market behaviour, you specifically must be curious about:

- How significant the SLR constraints have been as a factor in the recent Treasury market volatility

- Whether the current SLR framework needs reconsideration in light of these market events

And we know that the big investment banks have been calling for an easing of the SLR rule.

Note: The SLR came into effect in 2018 and was temporarily suspended during the Covid crisis.

Bottom Line:

SLR binds balance sheets, even for ultra-safe assets like Treasuries. In moments of stress, when the government and investors want banks to be the buyer of last resort, SLR does the opposite - it discourages them from stepping in.