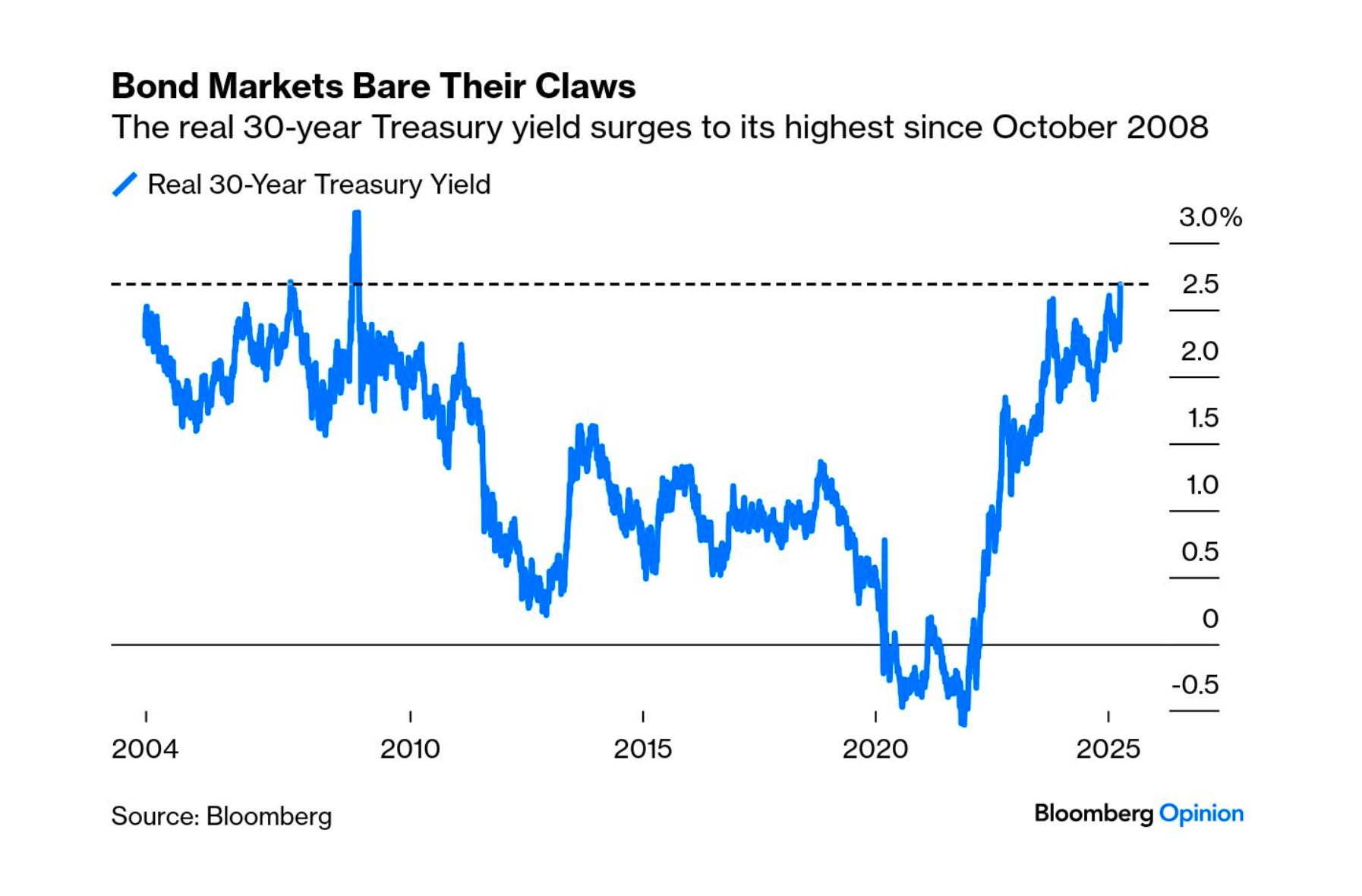

UST sell-off: From Safe-Haven to Lost-Haven?

Banks and How US Treasuries Take up Space & Capital

In the realm of Trump tariffs shades, the global asset markets are facing rising bond yields, falling stocks and a weakening USD.

The USD has been tumbling on concern its status as the world’s reserve currency is being eroded as the US-China trade war intensifies.

On top, this week, there was an apparent contradiction between the UST market and Fed rate cut expectations.

The UST sell-off went hand in hand with the increased rate cut expectations.

The unusual situation reflects a complex market dynamic that can be explained by several factors:

Term premium vs rate expectations:

The UST sell-off is likely driven by rising term premiums (the extra yield investors demand for longer-dated bonds beyond expected short-term rates), rather than by changing views on the Fed's path. This means investors want more compensation for holding longer-term debt, even while still expecting rate cuts.

Inflation concerns:

Markets might be pricing in more rate cuts due to economic growth concerns due to the significant rise in effective tariff rate, but simultaneously demanding higher yields on longer-dated UST due to persistent inflation worries. This creates a situation where short-term rate expectations can fall while long-term yields rise.

Supply-demand imbalance:

The UST market is facing significant supply pressure from large federal deficits requiring substantial UST issuance. Even if rates are expected to fall, this «supply glut» can push yields higher across the curve.

This situation highlights that Treasury yields are influenced by multiple factors beyond just Fed policy expectations, including supply-demand dynamics, inflation expectations, and risk premiums.

The market may be pricing in both economic weakness (justifying rate cuts) and persistent inflation or fiscal concerns (driving term premiums higher).

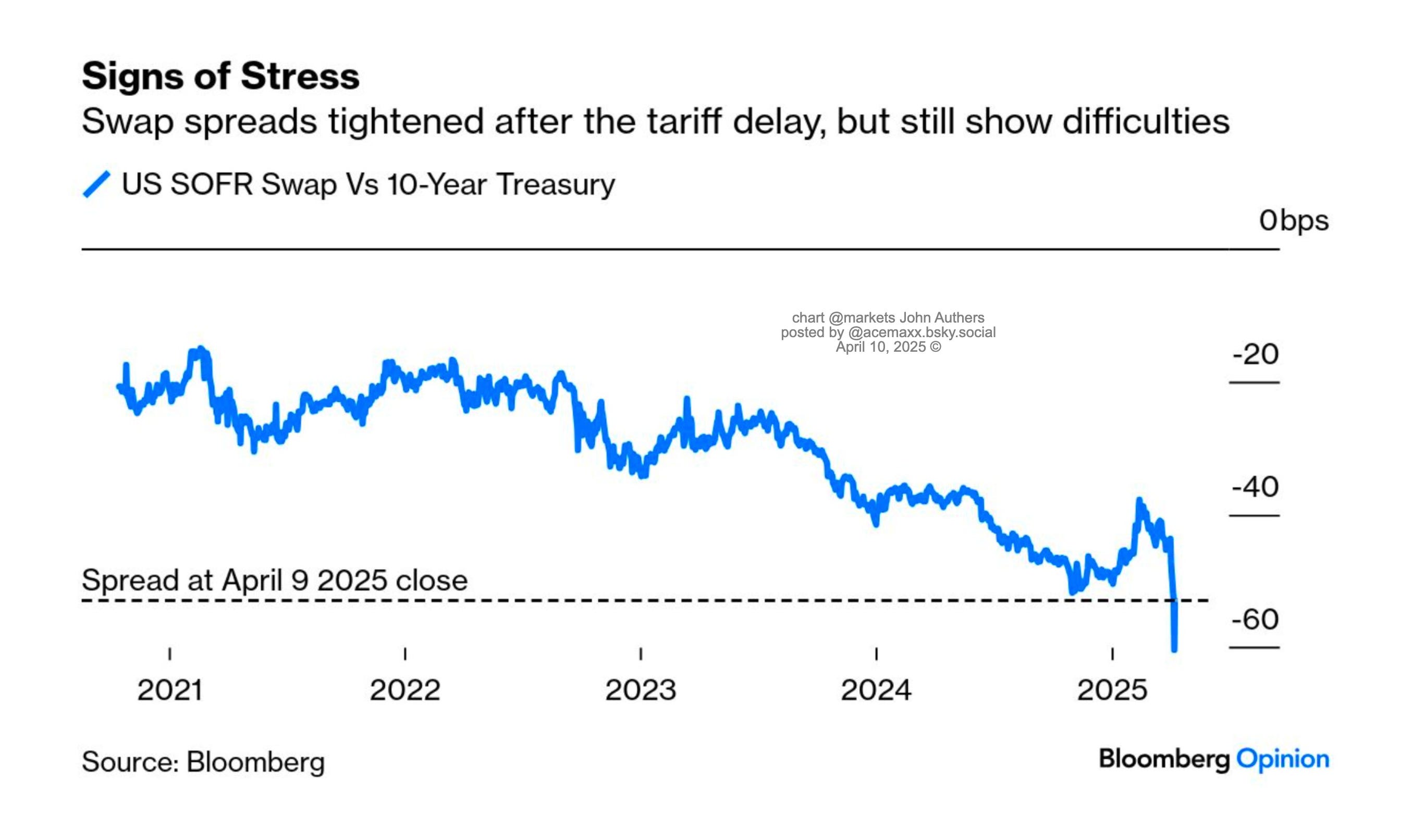

A negative spread between the US SOFR swap rate and 10y UST yield is also an unusual but increasingly relevant signal in modern rate markets.

Let’s break down what it means, how to interpret it, and what to watch for.

10y SOFR swap rate is the fixed rate on a plain-vanilla interest rate swap where one party pays fixed and the other receives floating SOFR (Secured Overnight Financing Rate).

10y UST yield is the yield on the benchmark 10y UST note.

The spread = SOFR swap rate – 10y Treasury yield

Normally this spread is positive, reflecting:

Credit/liquidity premium embedded in swaps,

Demand for Treasuries as "safe haven" assets,

Dealer balance sheet costs (swaps are often cleared; Treasuries “take balance sheet space”).

When this spread turns negative, it suggests:

“risk-off” mood, flight to safety,

Rate volatility or convexity hedging distortions,

Swap markets can price in rate cuts “more aggressively” than Treasury markets.

Which means:

Traders might be paying fixed in swaps to front-run Fed easing.

This drives swap rates below the Treasury curve.

It is furthermore interesting to try to dig the dealer balance sheet constraints:

Banks are unwilling to hold more Treasuries due to regulatory costs (SLR, Basel III).

Meanwhile, swap markets (cleared) are more efficient and cheaper to trade.

But what are balance sheet costs?

Every large bank (especially primary dealers) has a limited amount of balance sheet space.

Think of it like cargo space on a plane, there's only so much stuff you can carry, and some cargo is heavier (costlier) than others.

Banks have to follow strict rules about:

Leverage (e.g., Supplementary Leverage Ratio or SLR)

Risk weights on assets (under Basel III)

Liquidity coverage and capital charges.

This makes it expensive for them to hold certain assets, even if those assets are ultra-safe — like USTs.

This “regulatory imbalance” pressures swap spreads lower, and in some cases into negative territory (i.e., swap rates < UST yields).

By the way, watch these alongside:

SOFR-OIS curve steepness

Treasury repo rates (tightness signals demand for collateral)

USD cross-currency basis

Agency MBS spreads (convexity hedging pressure)

Fed Funds futures curve (expectations of cuts)

Bottomline

Even though Treasuries are risk-free, they still “consume balance sheet” under regulations like SLR.

This means holding lots of Treasuries requires banks to set aside capital.

If banks are constrained, they may demand higher yields on Treasuries to compensate - pushing Treasury yields up relative to swaps.