Why does the ECB keep Interest Rates higher than GDP growth?

Pointless “Debt-Brake” – Beyond “Zeitgeist”

When a central bank keeps interest rates above the economic growth rate, it's often a deliberate attempt to cool down an overheating economy and curb inflation.

However, it also carries the risk of slowing down economic activity and potentially triggering a recession.

We are talking about the ECB.

The ECB still has a restrictive monetary policy stance and makes no secret of this, as it most emphatically underlined on March 6.

“Monetary policy is becoming meaningfully less restrictive”

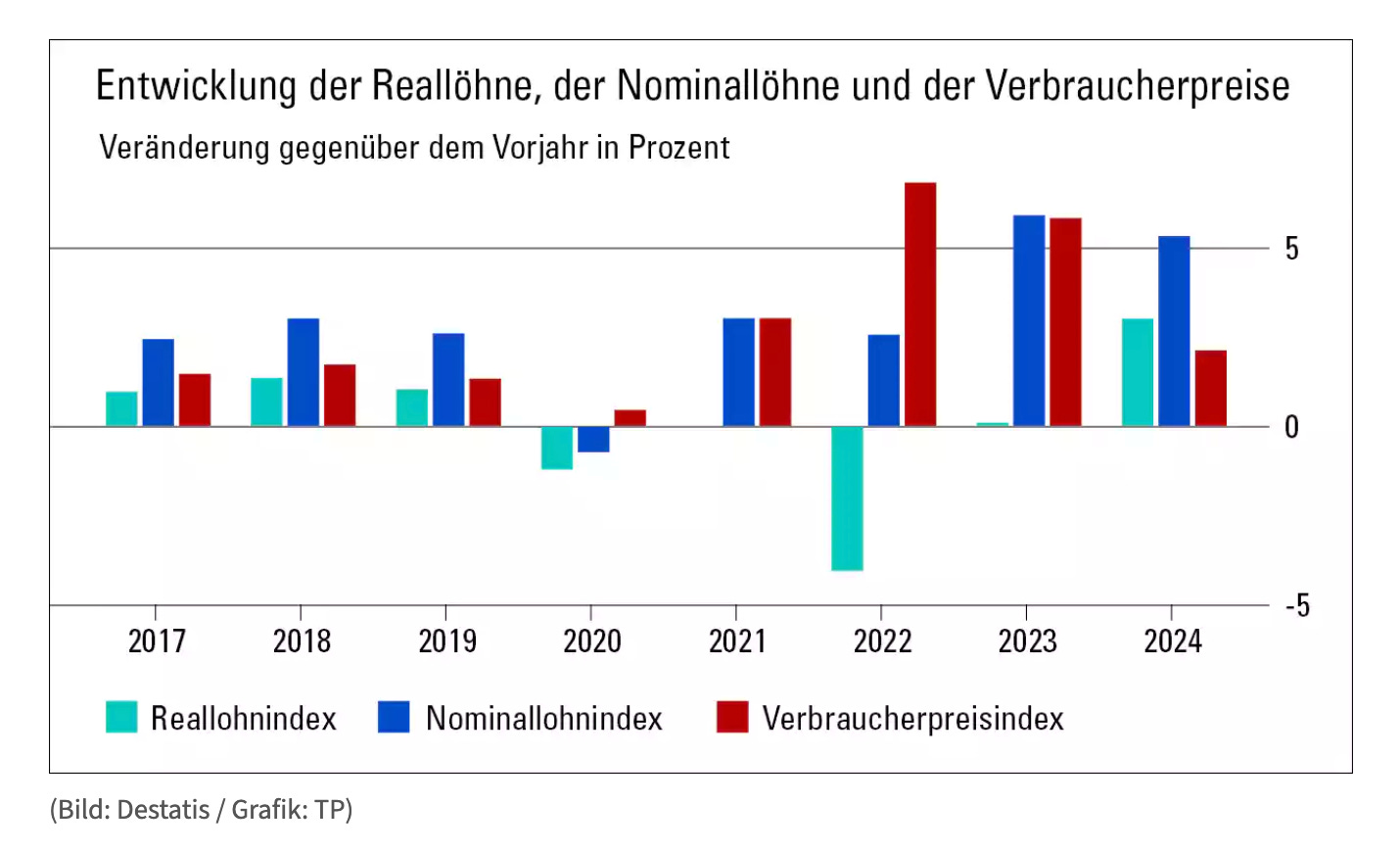

In the fourth quarter of 2024, seasonally adjusted GDP increased by 0.1% in the euro area and by 0.2% the EU, compared with the previous quarter. And the annual inflation rate in the euro area was 2.3% in February 2025.

This means that the ECB is fighting 0.3% inflation with all its might, while the German economy has been stagnating for three years.

Does that make sense?

When a central bank's policy rate exceeds the economy's GDP growth rate, several potential economic implications arise:

Increased Debt Burden:

Higher interest rates can lead to increased debt servicing costs for both governments and private entities. If the interest rate surpasses the GDP growth rate, the relative debt burden may grow over time, as the economy's capacity to generate income lags behind the accumulating interest obligations.

Reduced Investment:

Elevated policy rates can dampen investment by increasing borrowing costs, potentially slowing economic growth further.

Monetary Policy Considerations:

Central banks may face challenges in stimulating the economy if high policy rates persist, especially when inflation is low.

It is obvious that the magnitude of these effects depends on the difference between the interest rate and the growth rate, as well as the overall economic conditions.

To give a broad hint:

German PPI has been falling steadily over the past 20 months, at least 16-times in a row.

On Thursday, Swiss National Bank SNB cut the policy rate by 0.25% to 0.25%, on the grounds that 1) low inflationary pressure and 2) the heightened downside risks to inflation. And Swiss policy makers have delivered a new inflation forecast for 2025: 0.4%, 2026: 0.8% and 2027: 0.8%, all staying below 1%.

For a company that is willing to invest, the interest rate is the most important, the decisive factor. One way to determine the average return of the company is the growth rate of the economy, as Heiner Flassbeck recently pointed out.

It’s an open secret that the interest rate in relation to the economy in the euro area is far too high today. Many people complain about zero interest rates, but where is the higher interest rate supposed to come from if the growth rate of the economy is zero?

If monetary policy is wrong (misguided), then the Government must borrow and invest. There is no way around it.

The abolition of the totally pointless “debt brake” (“Schuldenbremse”, which is not aligned with the “Zeitgeist”) is a step in the right direction.

PS: Germany's plan for a massive ramp-up in defence and infrastructure spending will be a "positive" for its prized triple-A sovereign credit rating, S&P Global said a couple weeks ago.

"Our biggest concern with Germany's creditworthiness is the stagnating economy, so anything to boost the domestic economy is a credit positive”

S&P added that Germany's low debt levels meant it had "significant" room for additional spending, saying: The triple-A rating is safe.