Presidential Pressure on Fed – Trump Hammers Powell

Did Tariffs Delay Interest Rate Cuts?

It is now common public knowledge that Trump has repeatedly called on Fed Chairman Jerome Powell to lower interest rates in order to stimulate lending.

Lower interest rates make loans cheaper for private individuals and companies.

Trump did not stop at insults either. Most recently, he called Powell, whose term as Fed chairman ends next year (May 2026), a “numbskull”.

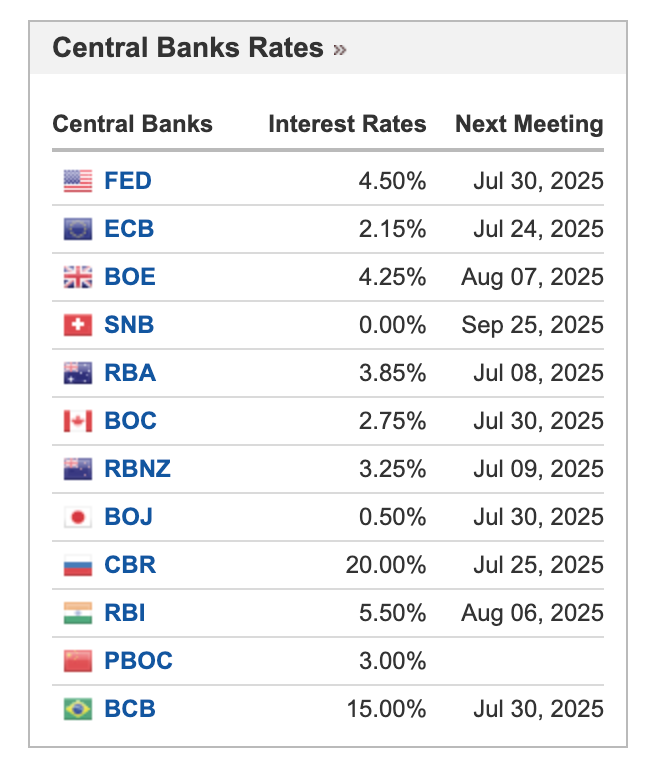

Yet, despite repeated calls from US President Trump to cut interest rates, the US Federal Reserve (Fed) has withstood pressure from the government and left the key interest rate at a high level in the range of 4.25 to 4.5%.

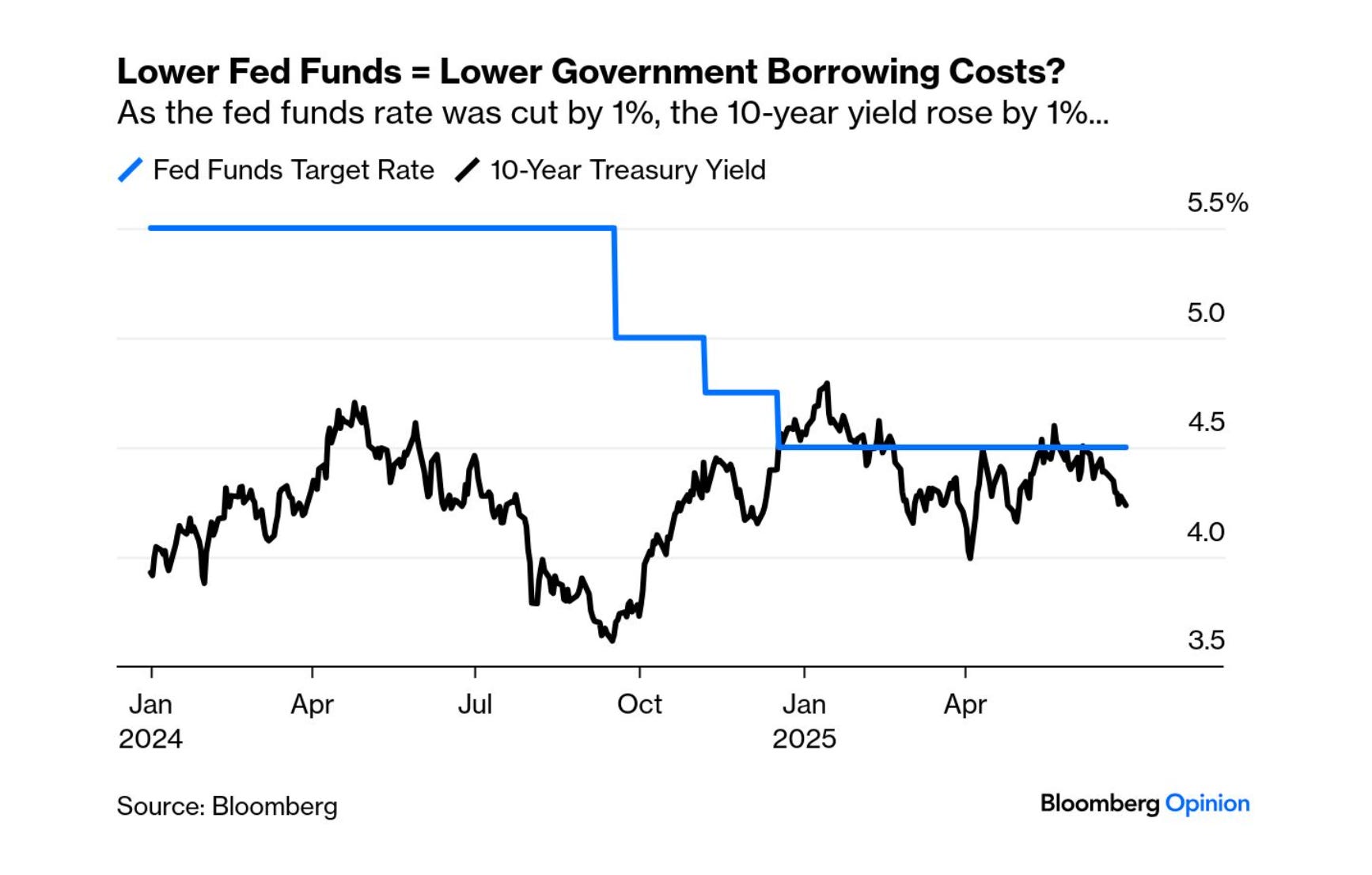

The question that cuts right to a core issue in monetary-fiscal dynamics is: How closely does the Fed funds rate influence long-term US government borrowing costs?

The claim that “lower Fed funds rate = lower government borrowing costs” is partially true, but not guaranteed - especially when it comes to long-term borrowing costs, like the yield on 10y UST bonds.

Because government borrowing costs vary by maturity:

Against this backdrop, it is worth recalling some historical evidence.

(1) Greenspan’s «Conundrum» (2004-2006).

Fed hiked short-term rates from 1% to 5.25%.

But 10y UST yields stayed flat, around 4.5%.

Why? The prevailing narrative at the time «global savings glut», China buying USTs, low inflation expectations.

The lesson is that long-term rates can ignore the Fed if the market sees long-term disinflation or safe-haven demand.

(2) 2023 inversion surprise.

In 2023, the Fed started to cut rates.

But 10y yields rose, not fell - by almost 100bp.

Why? Markets feared persistent inflation, fiscal dominance, and bond supply/demand imbalance.

The lesson is that a rate cut can even raise long-term yields if the market sees it as inflationary or debt-driven.

But when is the claim realistic?

It’s realistic only if:

Inflation expectations are stable or falling,

The market believes the Fed will stay dovish for long,

There’s strong demand for USTs.

Otherwise, long-term yields may rise on rate cuts, especially if:

The market expects higher future inflation,

There's fear of fiscal slippage or bond oversupply,

The Fed appears to be politically pressured (undermining credibility).

Note: long-term interest rates depend on future short-term rates, largely determined by expectations of future monetary policy targets (Prof L. Randall Wray).

Bottom Line:

"lower Fed funds rate = lower government borrowing costs" is only realistic for short-term borrowing costs (like T-bills),

but not reliable for long-term borrowing costs (like 10y or 30y bonds),

because bond yields reflect market expectations, not Fed diktats.

So yes - history shows that rate cuts can coincide with rising long-term yields. Trump's logic may work for short-term fiscal math, but not for locking in lower long-term debt financing.