It’s Time to Retire “Bond Vigilantes” Myth

A colourful metaphor, not an economic law

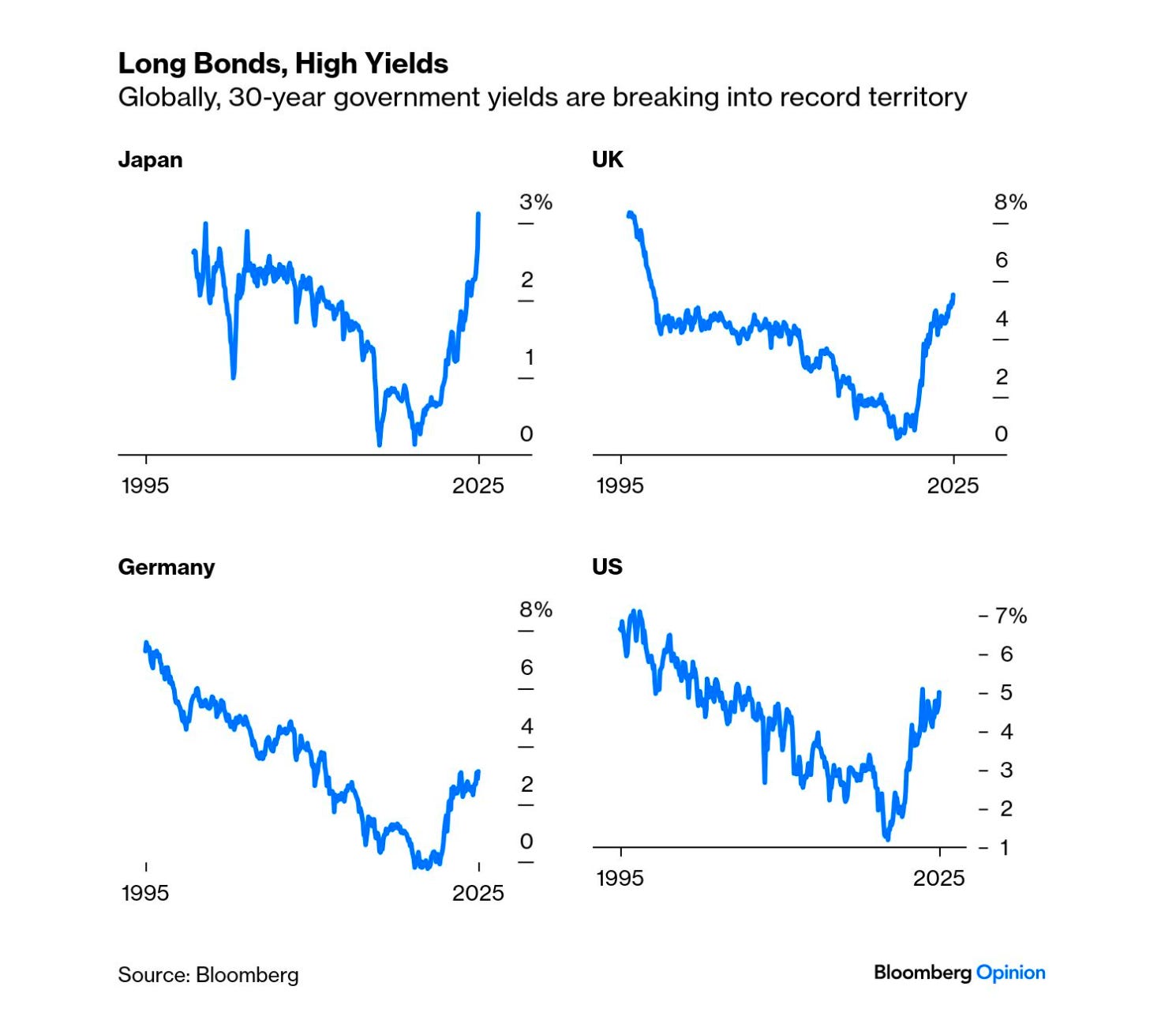

The term “bond vigilantes” has made a comeback in headlines, as rising yields spark talk of markets punishing governments for excessive borrowing.

But this colourful metaphor - coined in the 1980s - no longer reflects the complex reality of global bond markets.

This narrative is tempting, especially as long-end yields break above 5%, but it badly misrepresents how bond markets actually function today.

It's time we stopped treating it as economic gospel.

The idea that investors can collectively “discipline” governments by selling off bonds assumes a level of coherence, intent, and power that markets simply don’t possess. Bond markets are not a unified voice of reason.

They are shaped by a mix of expectations, hedging strategies, regulatory constraints, and - most importantly - central bank policies.

In an era of quantitative easing (QE) and massive central bank balance sheets, the notion of «market discipline» has been fundamentally altered.

For over a decade, despite record-high deficits in the US, UK, and Japan, bond yields remained historically low. No vigilantes in sight. What ultimately moved yields wasn’t spending, but inflation - and even then, not without hesitation.

If policymakers base decisions on fear of fictional vigilantes rather than on economic fundamentals, they may repeat the mistakes of “expansionary austerity” and underinvestment.

What bond markets actually demand is clarity, consistency, and credibility - not punishment.

Invoking “vigilantes” can be damaging in times when fiscal stimulus is needed, such as during recessions or crises.

It’s time to retire the vigilante myth.

Let’s start treating bond markets less like sheriffs and more like the complicated, ambivalent institutions they really are.