Fiscal Dominance in the Offing?

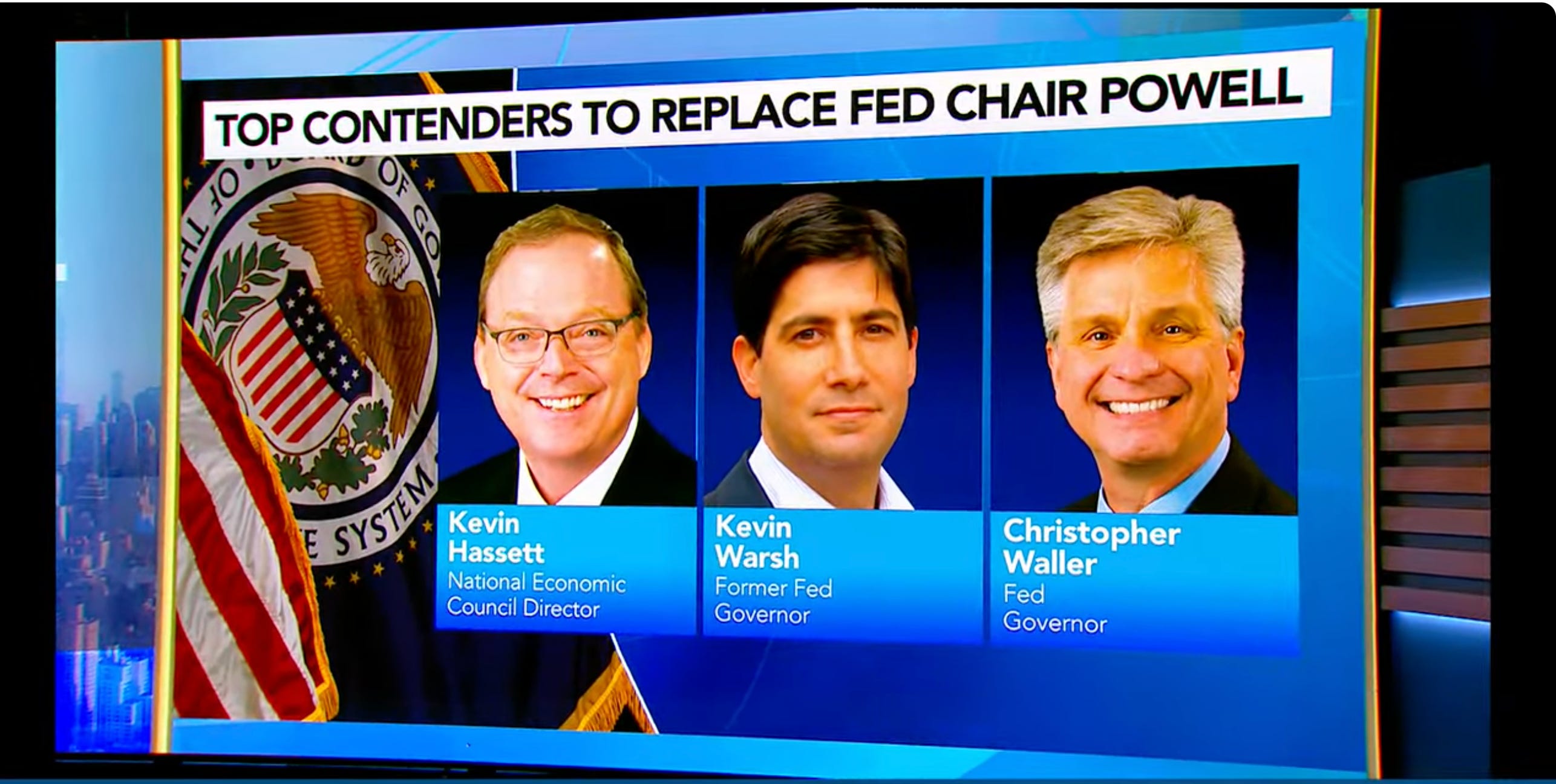

Kevin Warsh: The new Fed Chair?

Kevin Warsh’ call for a “regime change” and closer partnership between the Fed and Treasury indeed raises flags around the concept of fiscal dominance - a term that has very specific and serious implications in monetary economics.

Note: Warsh, former Fed Governor, is considered one of the 3 finalists to take over at the Fed. He is reportedly on President Trump’s short list to lead the institution.

Let’s break this down and assess whether Warsh's comments are heading in that direction.

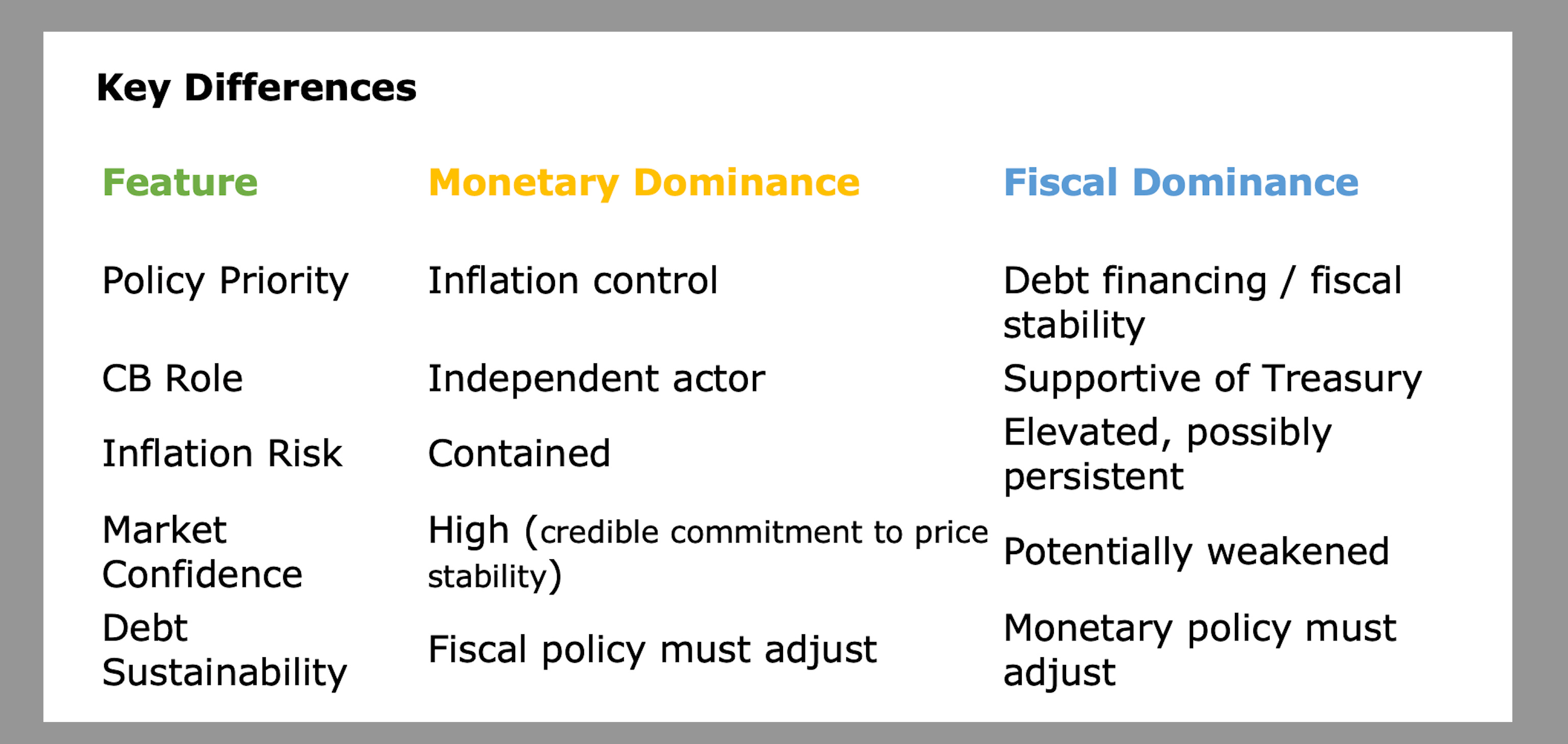

What Is Fiscal Dominance?

Fiscal dominance occurs when monetary policy becomes subordinate to fiscal needs - meaning the central bank adjusts its interest rate, balance sheet, or inflation tolerance to help the government manage debt or finance deficits, rather than pursuing its own goals (e.g., inflation control, full employment).

In such a regime, central banks may:

Keep interest rates low to reduce debt servicing costs

Monetize deficits via QE-style purchases

Delay tightening even in the face of inflation

This can lead to higher inflation risks, loss of central bank credibility, and long-term financial repression.

What Did Kevin Warsh Say?

Based on reports (like CNBC’s coverage), Warsh is calling for:

A “regime change” at the Fed, implying dissatisfaction with the current inflation-targeting framework or independence model.

A closer Fed-Treasury partnership, possibly to coordinate policy more tightly in the face of persistent supply shocks, geopolitical risk, and debt dynamics.

While he hasn’t explicitly advocated for fiscal dominance, his phrasing leans in that direction. The idea of institutional coordination sounds pragmatic - but it risks crossing a red line into politicizing the Fed’s decisions.

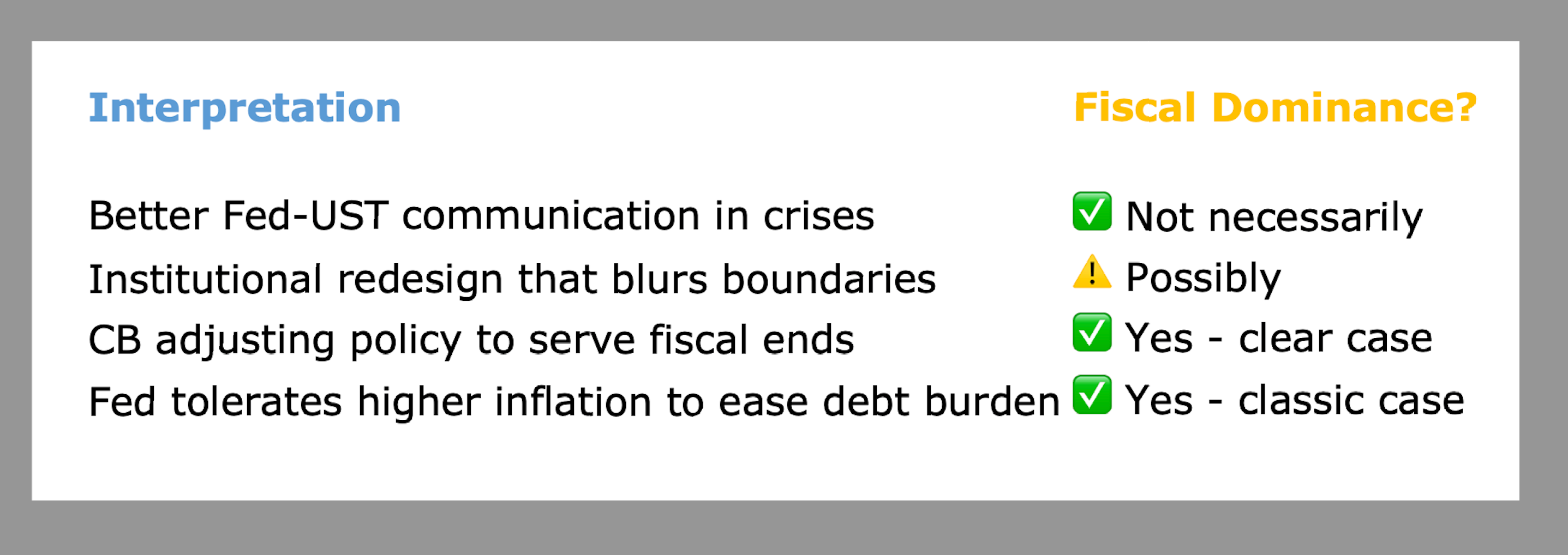

Is this fiscal dominance?

It depends on interpretation and intent:

So far, Warsh seems to be flirting with fiscal dominance language, but hasn’t crossed the line overtly. However, his criticism of the current Fed regime and call for a new framework could mean:

Less emphasis on pure inflation targeting

More attention to financial stability and debt sustainability

A tilt toward fiscal-monetary coordination, especially under rising debt-to-GDP levels

That moves the needle toward fiscal dominance, if not quite embracing it.

Historical and Global Parallels

In the 1940s, the Fed was explicitly under UST control to keep borrowing costs low during WWII - a textbook fiscal dominance period.

In Japan, the BoJ's long-term Govt bond purchases and yield curve control resemble fiscal support tools.

In emerging markets (EM), fiscal dominance is more common and often leads to inflation instability or capital flight.

Bottom Line

Warsh’s framing of “regime change” and “Treasury partnership” may be designed to sound bold and reformist, but it walks uncomfortably close to fiscal dominance.

If such a policy shift comes from the top of the Fed, it risks undermining:

Market expectations of Fed independence

The Fed’s ability to fight inflation credibly

The US dollar’s role as a store of value

To be clear, Fed independence does not just mean independence to slow the economy during periods of inflation. This independence also helps them ignore calls to tolerate crisis levels of unemployment.

Ironically, some of the names being floated to replace Jerome Powell in the event of a firing are people who savagely criticized the Fed for trying to bring down crisis levels of unemployment in the 2010s, even as inflation remained historically low.

as Josh Bivens, Economic Policy Institute (EPI) calls to mind.

They are unserious partisan hacks.

If Warsh becomes Fed Chair, expect more debate about what independence means in an emerging unilateral world - and whether the Fed's role will quietly evolve into supporting the Treasury’s position, not just price stability.

Note: The balance between these regimes often shifts during different economic periods, with monetary dominance more common during stable times and fiscal dominance emerging during major crises or when governments face severe debt constraints.