Fed Financial Stability Report

The excess bond premium

On Friday, Fed has published their «Financial Stability Report” May 2026.

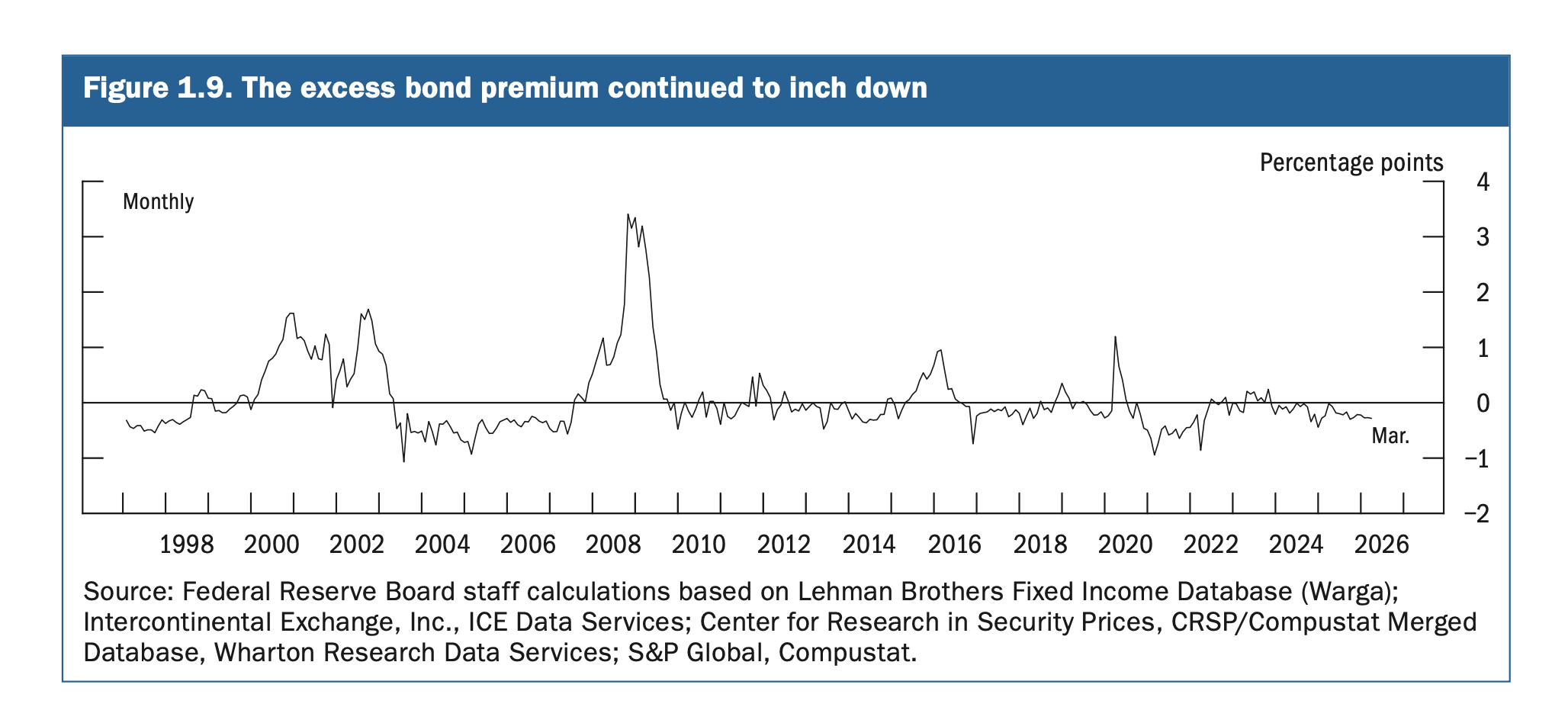

«The excess bond premium for all nonfinancial corporate bonds - a measure of the risk premium required by bond investors after controlling for bond characteristics and credit quality—continued to edge down and remained below the median of its historical distribution».

This is one of those phrases that sounds technical but actually captures something very intuitive about market psychology.

What exactly is meant with “risk premium required by bond investors” is down?

Is it good or bad for the financial markets or the economy in general?

When investors buy corporate bonds, they demand compensation for risk. That compensation has two layers:

(a) “Fundamental” risk (credit risk)

(b) The extra premium (this is the key part)

The “excess bond premium” mentioned by the Fed tries to isolate something beyond fundamentals: How much extra return investors demand just because they feel cautious or risk-averse.

So:

• If investors are nervous, they demand high extra compensation

• If investors are relaxed, they accept low extra compensation

The “risk premium required by bond investors” = How much extra yield investors demand for bearing uncertainty and fear.

What does it mean that it is “down”?

If the report says: “the excess bond premium … continued to edge down” that means: Investors are requiring less extra compensation for risk.

So:

• Corporate bond spreads are tighter (after adjusting for fundamentals)

• Investors are more willing to hold risky debt

• Financial conditions are easing

Why does this happen?

Typically, this reflects:

(a) Strong risk appetite: investors feel confident about the economy

(b) Abundant liquidity / low rates: safe yields are low; investors “reach for yield”

(c) Stable macro environment (or perceived stability): low volatility and predictable policy

Is this good or bad?

Here’s where it gets interesting. It’s both, depending on the perspective.

The “good” interpretation (short-term, cyclical view)

Lower risk premia mean:

Firms can borrow more cheaply

Investment becomes easier

Financial conditions support growth

This is typically positive for the economy in the short run

The “bad” interpretation (financial stability view)

From a financial stability perspective (which is exactly what the Fed report is about):

Low risk premia can signal complacency. In other words:

Investors may be underpricing risk

Credit spreads may be too tight

Leverage may be building quietly

Bottom line

When the Fed says the “risk premium required by bond investors is down,” it means:

• Investors are less cautious

• They accept lower compensation for risk

• Financial conditions are looser

Short term: supportive for growth.

Long term: could signal complacency and vulnerability.