ECB and the Cost of Underinvestment

Isabel Schnabel’s Speech: A Shift in Tone?

The inflation in the euro area is currently just below ECB’s target and is expected to slide further into 2026.

With this in mind, Philip R. Lane, a member of the Executive Board of the ECB, stated on Wednesday that

ECB’s rate cut on 5th June helps ensure that the projected negative inflation deviation over the next 18-months remains temporary.

It is furthermore remarkable that Isabel Schnabel, also a member of the Executive Board of the ECB told a seminar on Thursday that

the expected slowing of euro zone inflation, which the ECB forecasts at 1.6% in 2026 against 1.9% last month, was a temporary phenomenon, due to energy price base effects and the stronger euro exchange rate.

Schnabel, seen as one of the ECB's policy hawks, said in addition that

ECB interest rates are in a "good place" now, despite an expected slowing of inflation, because price growth is likely to return to the ECB's target of 2% over the medium term.

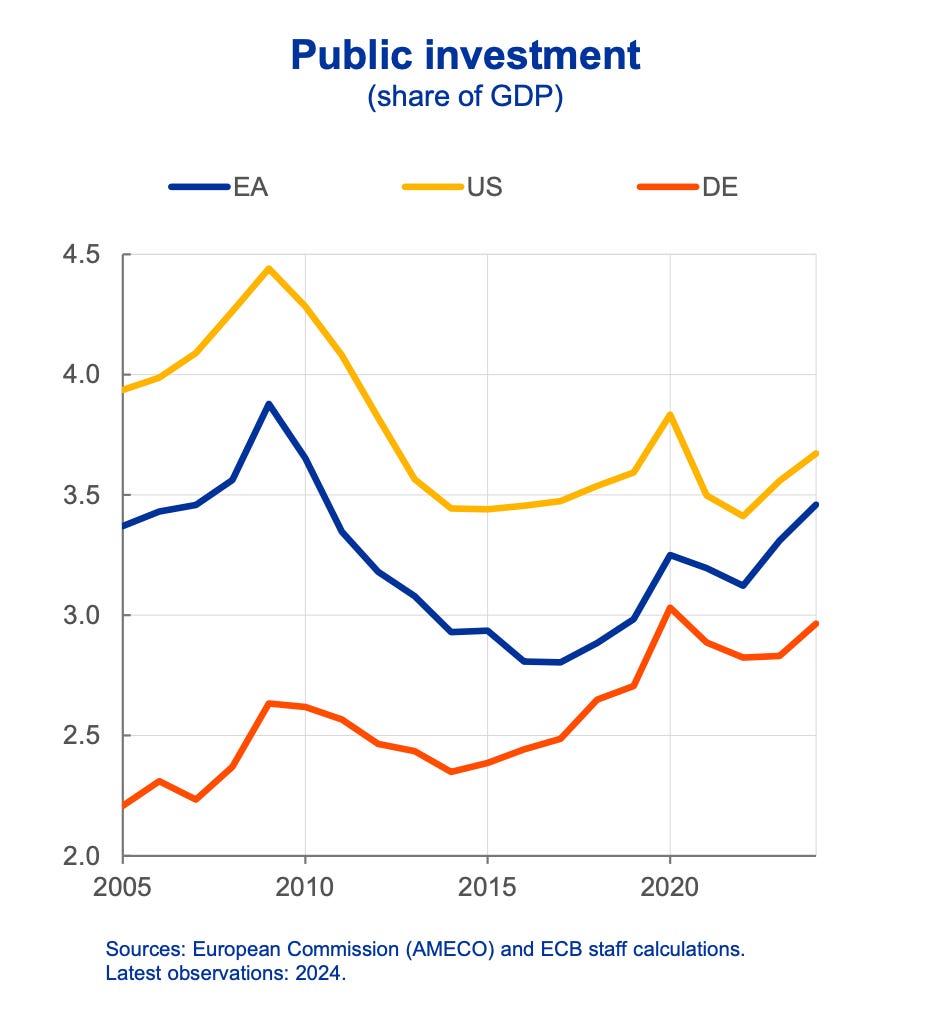

German economist’s statement that potential growth in the eurozone declined after the global financial crisis (2008) partly due to a lack of investment is unique.

This insight raises an obvious and pressing question:

Why, despite persistently low growth and low interest rates, has the level of public investment in the euro area remained below where it was 20 years ago?

The answer lies in the combined - and often self-defeating - effects of overly restrictive monetary policy in key moments and a fiscally conservative framework (austerity) dominated by rules such as the Stability and Growth Pact and national "debt brake."

Was ECB monetary policy too restrictive?

Yes - for much of the period following the GFC (2008), ECB policy was too tight relative to the economic situation.

The ECB raised rates prematurely in 2011 despite fragile recovery - a policy error widely criticized in hindsight.

Even after launching QE (quantitative easing) in 2015, the ECB remained reluctant compared to the Fed, partly due to political constraints.

ECB policy also lacked a coordinated fiscal counterpart - it was pushing on a string while governments cut spending.

To be fair: Monetary policy alone cannot stimulate public investment, especially when governments are actively cutting back.

Was fiscal policy (austerity, debt brake) the real culprit?

Yes - fiscal austerity, driven by Brussels and Berlin, played a dominant role in suppressing public investment.

The EU Stability and Growth Pact (SGP) and national “debt brake” rules (like Germany’s Schuldenbremse) forced governments to prioritize debt reduction over investment.

After the GFC, many countries cut public investment to meet deficit targets — this was the easiest spending item to reduce politically.

Why this matters:

Public investment is a key driver of potential growth (e.g., through infrastructure, R&D, education).

weak investment = weak productivity growth = lower future incomes

Isabel Schnabel’s recent remarks suggest the ECB now recognizes the long-run damage caused by underinvestment and fiscal over-caution.

This reflects a broader rethinking in Brussels and Frankfurt:

New EU fiscal rules (still debated) may allow more space for investment.

The ECB is more vocal about the limits of monetary policy and the need for fiscal action.

Yes - the low level of public investment in the euro area is largely due to fiscal austerity and the enforcement of tight budget rules.

ECB monetary policy was also too restrictive at key moments, but it was fiscal policy that cut the investment legs from under the economy - even when borrowing was nearly free.