Current Account Balance and «Savings Glut»

An Unbalanced Debate on Trade Unbalances

When it comes to explaining current account surpluses and deficits, mainstream-economists resort to the "savings glut" thesis.

But it somehow leaves the impression that it's just a description of what is happening, not an explanation. Moreover, it is certainly misleading to explain flows of goods with flows of capital.

Heiner Flassbeck is absolutely right to question the "savings glut" thesis which is often treated as a tidy explanation, but it’s really more of a label than a cause, and the approach of the former Chief of Macroeconomics and Development of the UNCTAD to push deeper is spot on.

What is the “Savings Glut” Thesis?

Mainstream economists (notably Ben Bernanke) use the term to argue:

Countries like China, Germany, or oil exporters save more than they invest, and those “excess” savings flow into deficit countries (like the U.S.), financing their current account deficits.

So, if the U.S. runs a current account deficit, it's not because it's irresponsible — it's because others are too responsible.

But here’s the issue:

It’s Descriptive, Not Causal

Saying “there’s more saving than investment” doesn't explain why that imbalance exists.

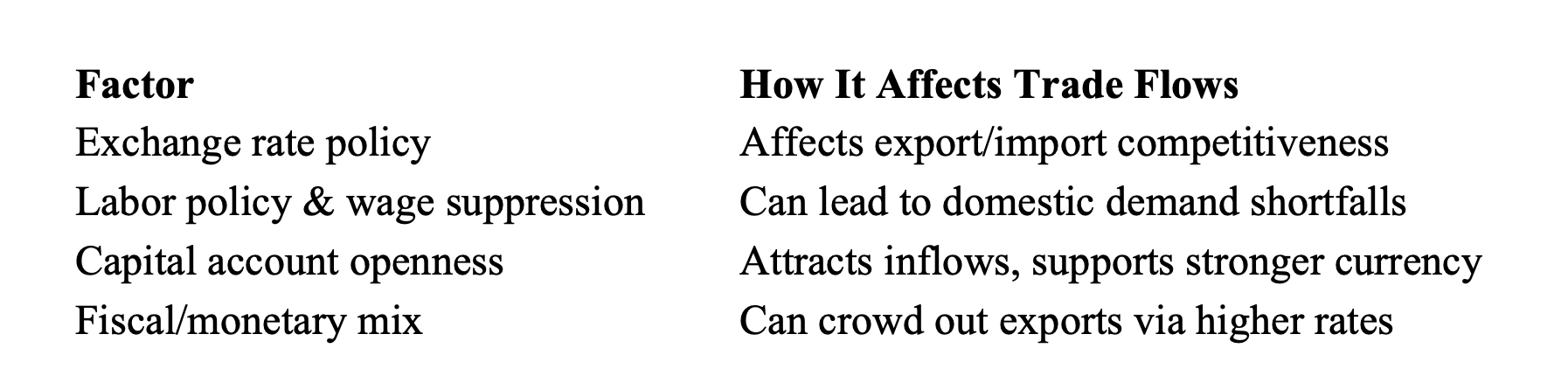

It doesn’t tackle structural drivers like trade policy, wage suppression, domestic underinvestment, or currency manipulation.

Confusing Flows of Goods with Flows of Capital

A current account deficit means: imports > exports.

The capital account surplus means: foreigners buy more U.S. assets (bonds, real estate, etc.).

But the causality is murky: are Americans importing too much, or are foreigners buying U.S. assets and thus pushing up the dollar, making imports cheaper?

Explaining trade imbalances with capital flows risks flipping cause and effect.

It Deflects Responsibility

The “savings glut” narrative shifts blame from domestic policies to global ones.

The bottom line is that “saving glut” is a symptom, not a cause.

To explain global imbalances, we need to dig into the institutional, policy, and structural choices that shape savings, investment, and trade dynamics.

For many people (including some mainstream economists) it is self-evident to think that saving must come before investment and deposits before bank loans. It is therefore tempting to see saving as the source of financing and the main driver of many macroeconomic developments.

Savings are not necessary to fund purchases or investment. The best way to fund savings would be for governments or private banks to issue new debt. Banks create deposits when they make loans. What we create, we can afford.

Note (agree to disagree): Even Michael Pettis seems to a support of the “Savings Glut” thesis as he says that «the idea that trade imbalances are more likely to be the result of credit imbalances than of savings imbalances ignores the role of savings imbalances in creating credit imbalances.»