America’s Debt Panic Is Misplaced

And Moralists Are Missing the Point

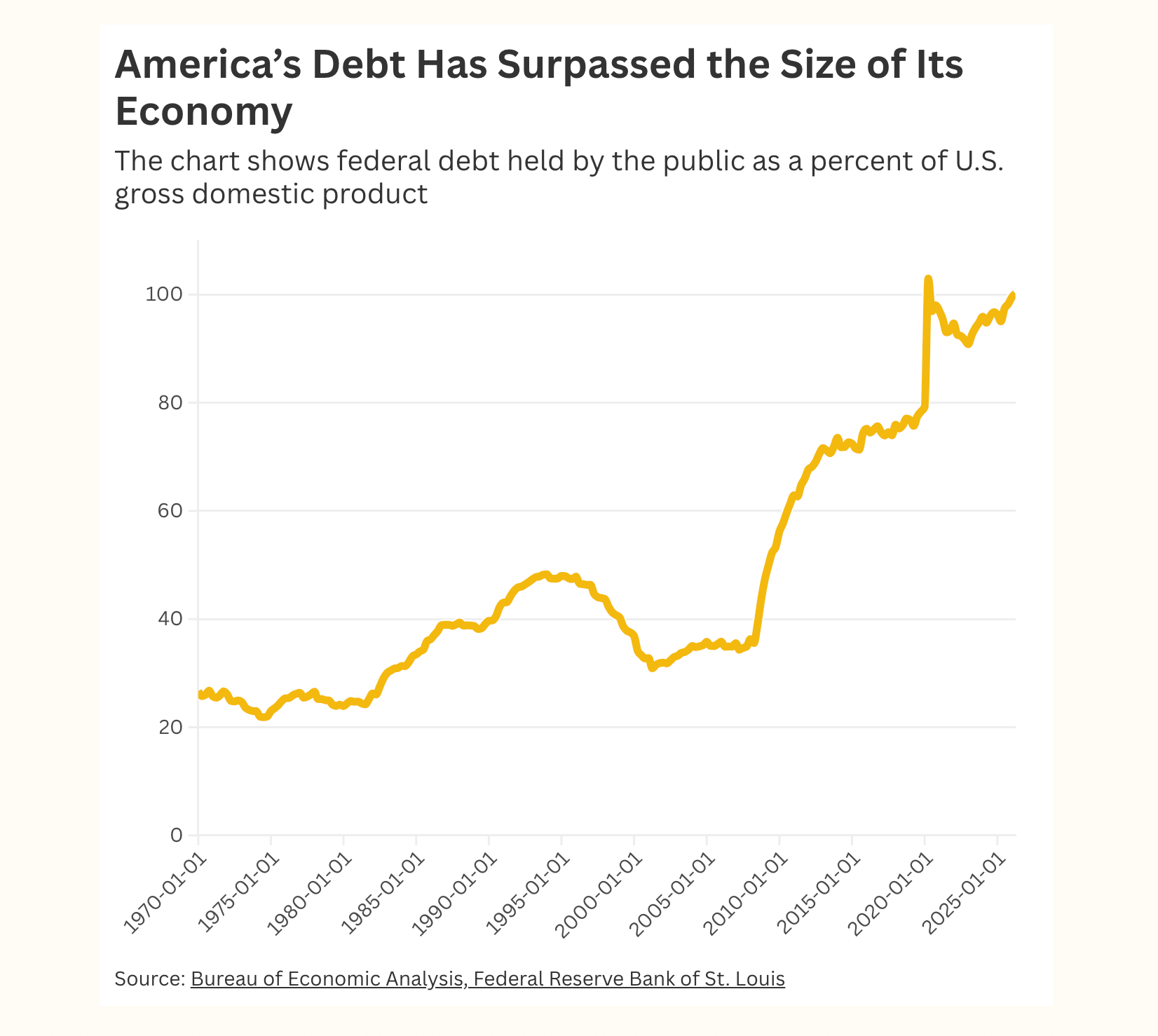

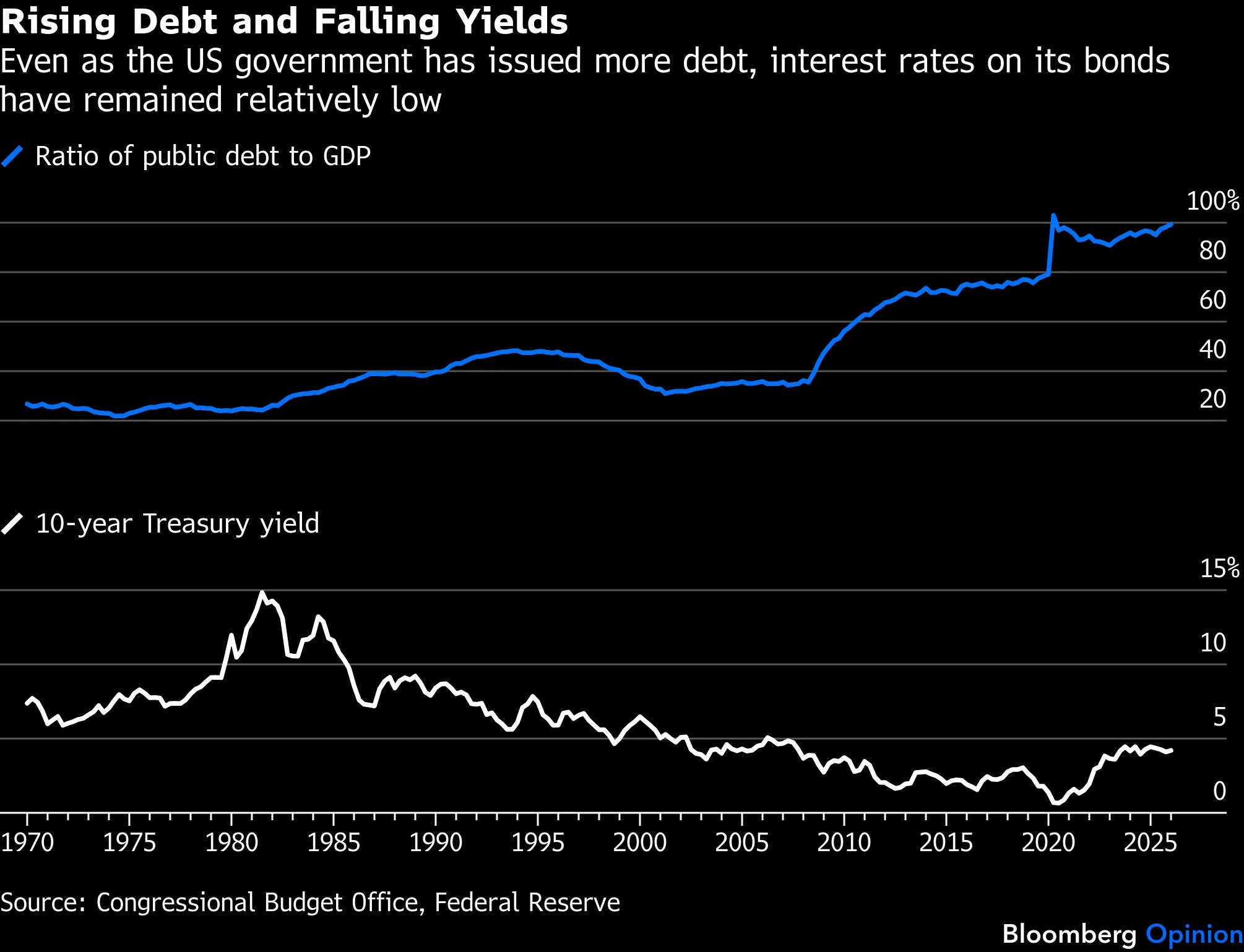

Every few months, a familiar headline returns: U.S. public debt has reached a new, supposedly alarming milestone—now exceeding the size of the economy itself. Rating agencies clear their throats, commentators rediscover their fiscal virtue, and the same tired analogy resurfaces: the government, we are told, must tighten its belt like a prudent household.

This is not just wrong. It is economically illiterate.

A sovereign state is not a household. It does not need to “pay back” its debt in the way a family must settle a mortgage. Public debt is continuously rolled over, functioning as a financial asset for the private sector. To frame it as a burden in the conventional sense is to misunderstand the basic architecture of modern monetary economies.

The United States, issuing debt in its own currency, cannot “run out of money.” The real constraint is not solvency, but inflation. If there is idle capacity, unemployment, or underused resources, public deficits are not only sustainable but necessary. They are the mechanism through which demand is stabilized and economic activity maintained.

So why the panic?

Because much of the debate is not about economics at all. It is about moralism. Debt is treated as a sign of excess, a deviation from virtue, a failure of discipline. Rating agencies - whose track record includes spectacular blindness before the global financial crisis (GFC) - position themselves as arbiters of fiscal responsibility. Yet their warnings are based on arbitrary thresholds and models that consistently fail to grasp the dynamics of real economies.

But rejecting debt hysteria does not mean embracing complacency. The real issue is not the level of public debt; it is whether macroeconomic policy is coherent.

First, inflation is not a simple byproduct of “too much spending.” It is fundamentally linked to wage dynamics. If nominal wages rise in line with productivity plus the central bank’s inflation target, price stability can be maintained even with sustained fiscal deficits. If wages are suppressed, economies stagnate. If they outpace productivity excessively, inflation emerges. The key variable is not debt—it is the relationship between wages and productivity.

Second, the relationship between interest rates and growth cannot be ignored. As long as economic growth matches or exceeds interest rates, the debt ratio stabilizes or declines naturally. If policymakers allow interest rates to rise above growth for prolonged periods, they create the very instability they claim to fear. This is not an iron law of markets but a policy choice—one that central banks have the power to influence directly.

Third, and most neglected in the American debate, is the external balance. The United States enjoys the privilege of issuing the world’s reserve currency, which allows it far greater “fiscal space” than other countries. But this does not mean that external imbalances are irrelevant. Persistent deficits in trade and competitiveness can, over time, constrain policy options in ways that no domestic fiscal rule can fix.

What follows from all this is straightforward: the obsession with debt ratios is a distraction. It diverts attention from the variables that actually determine economic stability—wages, productivity, interest rates, and external balances.

The irony is that the loudest calls for fiscal restraint often come at precisely the wrong moment. When private demand is weak, cutting public spending does not restore “confidence”; it deepens the downturn. Europe’s experience after 2010 should have settled this debate. It did not.

Instead of rehearsing moral narratives about debt, policymakers should focus on ensuring full employment, stable wage growth, and a coherent macroeconomic framework. If those conditions are met, the debt ratio will take care of itself. If they are not, no amount of fiscal virtue will prevent economic failure.